Each estate and trust situation is unique. Please consult a legal professional and/or tax professional before making any decisions or taking any actions.

If you’ve recently been named a trustee or executor of an estate, one of the first things that hits you is the paperwork. It’s a lot. And unlike a personal tax return, a trust or estate tax return involves a different set of rules, different forms, and a different kind of documentation.

This guide breaks down exactly what documents you’ll need to prepare a trust tax return in plain language, without the overwhelming legal jargon. Whether you’re working with an estate accountant or trying to get organized before your first meeting, this list will help you come prepared.

First, Understand What You’re Filing

A trust tax return is filed using Form 1041 (U.S. Income Tax Return for Estates and Trusts). This is separate from the estate tax return (Form 706), which deals with the overall value of the estate. Form 1041 covers income earned by the trust or estate during the tax year, things like rental income, dividends, capital gains, and interest.

If you’re managing an estate or trust in Orange County, this distinction matters. The rules around estate and trust tax can get complicated quickly, especially when significant assets are involved.

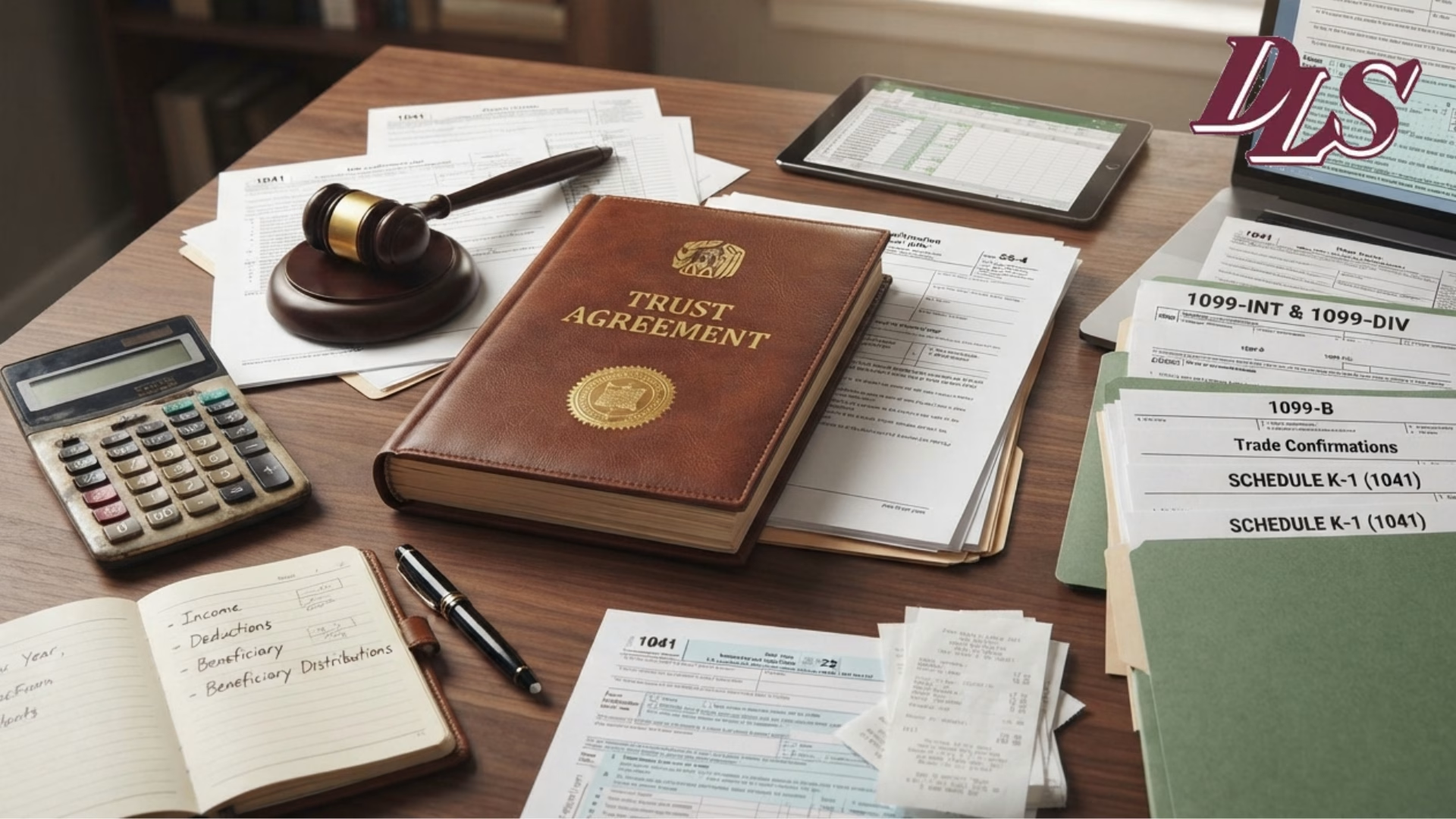

The Core Documents You’ll Need

1. The Trust Document or Will

This is the foundation of everything. The trust document (or the will, in the case of a probate estate) outlines the terms of who the beneficiaries are, how income and assets are to be distributed, and what powers the trustee or executor holds.

Your accountant for estate taxes will need this to understand the structure of the trust and confirm what rules apply. Without it, it’s nearly impossible to file accurately.

2. Taxpayer Identification Number (TIN) for the Trust

Trusts and estates have their own tax identification numbers different from the decedent’s Social Security Number. If the trust doesn’t already have a TIN, you’ll need to obtain one from the IRS using Form SS-4.

This number is required to open accounts, file returns, and receive any income on behalf of the trust.

3. Income Documents

Any income earned by the trust during the tax year needs to be reported. Gather the following:

- 1099 forms (for interest, dividends, retirement distributions, or proceeds from sales)

- K-1 forms (if the trust has ownership in a partnership, S corporation, or another trust)

- Rental income records (leases, rent payment histories, and expense receipts)

- Business income records (if the trust operates or owns a business)

This is one area where things can get complex fast. If the estate or trust has multiple income sources or investments, a trust accounting specialist can help make sure nothing gets missed.

4. Asset Inventory and Valuation

You’ll need a clear picture of what assets the trust or estate holds. This includes:

- Bank and brokerage account statements (from the date of death through the end of the tax year)

- Real estate records and appraisals (especially if the property was sold or transferred)

- Business ownership documents and valuations

- Vehicle titles and appraisals

- Retirement account records

- Life insurance proceeds documentation

For high-value estates, formal appraisals are often required. Accurate asset valuation is critical it affects both the trust tax return and potential estate taxes. This is especially true in Orange County, where real estate values alone can push estates into higher tax brackets.

5. Deductible Expenses

One of the advantages of trust and estate tax preparation is that many expenses are deductible. To take these deductions, you’ll need documentation for:

- Attorney and accountant fees paid during estate administration

- Trustee fees (compensation paid to the person managing the trust)

- Court and filing fees (particularly relevant in probate cases)

- Investment advisory fees paid by the trust

- Mortgage interest and property taxes on real estate held by the trust

- There are potentially other expenses not listed here that are unique to your circumstance.

Keep receipts and invoices. These deductions can meaningfully reduce the trust’s tax liability.

6. Distribution Records

If the trust made distributions to beneficiaries during the year, those distributions need to be documented. Distributions pass the tax liability to the beneficiary rather than the trust, which is an important planning tool.

You’ll need:

- Written records of all distributions made to beneficiaries

- Beneficiary information (names, addresses, and Social Security numbers)

This is something many trustees overlook early on. A qualified estate accountant will make sure the K-1s are prepared accurately and filed correctly.

7. Prior Year Tax Returns (If Applicable)

If the trust has been in existence for more than a year, bring prior year returns. These help identify carryover items like capital loss carryforwards that affect the current year’s tax picture.

They also help your tax preparer spot inconsistencies or potential issues before they become problems.

8. Probate Court Documents (If Applicable)

If the estate is going through probate, you’ll need documentation from the probate court. This typically includes:

- Letters testamentary or letters of administration (proof of your legal authority to act on behalf of the estate)

- Inventory filed with the court

- Any court orders related to the distribution or sale of assets

For probate accounting in Orange County, this documentation forms the basis of the financial record you’ll need to present to the court. The court requires an accurate, detailed accounting of all transactions, receipts, disbursements, and asset movements.

A Note on Timing

Trust tax returns are typically due on April 15, the same as individual returns, though extensions are available. For fiscal-year trusts, the deadline falls on the 15th day of the fourth month after the end of the fiscal year.

The earlier you get organized, the smoother the process. Trustees and executors who wait until the last minute often find themselves scrambling for documents and sometimes facing penalties for incomplete or inaccurate filings.

Why Working With a Specialist Matters

Estate and trust tax is a niche area. It’s not the same as filing a regular personal return, and not every CPA has the experience to handle it well. The documentation requirements are detailed, the rules around distributions are specific, and the stakes, particularly for high-value estates, are significant.

At Donna L. Stern CPA, APC, we’ve been handling estate and trust tax in Orange County for over 40 years. We work with trustees, executors, and the attorneys who represent them. We know the local tax environment, we understand probate accounting requirements, and we take a hands-on approach with every client.

If you’ve been handed the responsibility of managing a trust or estate, we can help you get organized, stay compliant, and protect the assets that matter to your clients and their families.

Getting Started

The best thing you can do before your first meeting with an estate accountant is gather as many of the documents listed above as possible. Even if you don’t have everything, coming in with what you have gives your accountant a starting point and helps avoid delays.

If you’re looking for an experienced accountant for estate taxes in Orange County, we’d be glad to help. Reach out to Donna L. Stern, CPA, APC, to schedule your free 30-minute consultation.

By submitting a form, calling us, or emailing us you consent to receive SMS messages in regards to appointment reminders, office directions, feedback requests, and other relevant communications. I understand that message and data rates may apply and that I can opt out at any time.

Disclaimer

The content on this web site is for informational purposes only. Nothing on this website should be construed to be tax/accounting advice, and you should not act or refrain from acting on the basis of any content on this site without seeking appropriate tax/accounting advice regarding your particular situation, from a licensed Certified Public Accountant in your state. The content on this site is not guaranteed to be correct, complete, or up to date.

The office of Donna L. Stern CPA, APC. is in Orange County, California and is only licensed for tax/accounting services in California. Please be advised that Donna L. Stern CPA, APC. only provides tax/accounting services or advice pursuant to a written tax/accounting services agreement. The content on this website is not intended to, and does not, create a CPA-client relationship between you and Donna L. Stern CPA, APC., nor does our receipt of an email or other communication from you.

Some jurisdictions may consider this site to constitute tax/accounting advertising; accordingly, please be advised this is an advertisement. Hiring a Certified Public Accountant is an important decision that you should not make based solely on advertising or on our self-proclaimed expertise. Rather, you should make your own independent evaluation of any Certified Public Accountant who you are thinking about hiring.

Testimonials or endorsements do not constitute a guarantee, warranty or prediction regarding the outcome of your tax/accounting matter. The result portrayed in any testimonials or endorsements were dependent on the facts of that case, and the results will differ if based on different facts. Donna L. Stern CPA, APC. does not offer any guarantees with regard to the outcome of your matter. Prior results in other cases do not guarantee a similar outcome in your case.

IRS CIRCULAR 230 DISCLOSURE: To ensure compliance with requirements imposed by the IRS, we inform you that, to the extent this communication (or any attachment) addresses any tax matter, it was not written to be (and may not be) relied upon to (i) avoid tax-related penalties under the Internal Revenue Code, or (ii) promote, market or recommend to another party any transaction or matter addressed herein (or in any such attachment).

By submitting a form, calling us, or emailing us you consent to receive SMS messages in regards to appointment reminders, office directions, feedback requests, and other relevant communications. I understand that message and data rates may apply and that I can opt out at any time.